Insurance is a pillar of contemporary financial systems: lenders typically require coverage to secure mortgages, and firms rely on insurance for risk management that protects not only asset values but also income streams. In a world with intensifying climate hazards, property insurance has become critical for both residential and commercial real estate, providing liquidity and financial resilience when disasters strike, enabling recovery and adaptation (Shi and Moser, 2021).

Over the last two decades, there has been an intensification in the frequency and severity of natural disasters, leading to greater economic losses. This rise in losses has placed insurance companies and reinsurers under severe stress. The result: the framework that supports insurers for commercial landlords and homeowners is coming under strain. Insurers have responded by sharply raising premiums, tightening terms, or withdrawing from high-risk markets.

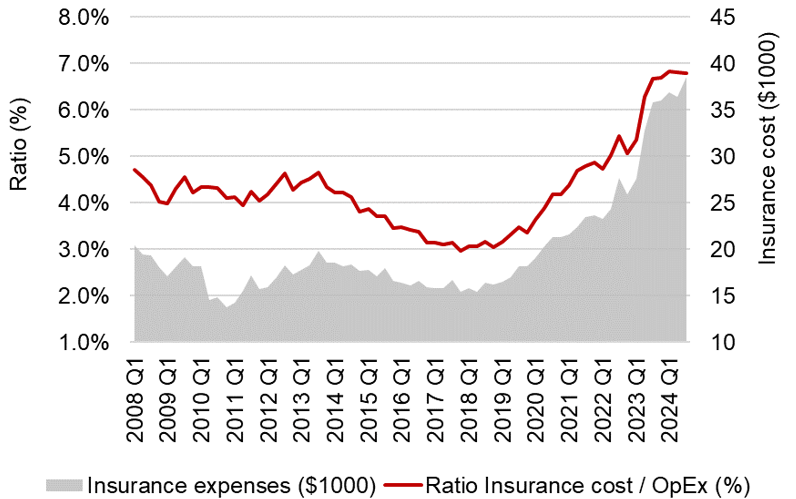

For commercial real estate investors, it has become essential to understand how resilient the insurance ecosystem is in a world of increasing physical climate risk. Extreme weather events have driven up economic losses, which in turn have pushed premiums higher and potentially translated into rising insurance costs that erode the profitability of CRE investments. Recent evidence investigates the scale of this impact (Figure 1). Commercial properties in the U.S. located in hurricane-affected areas have experienced an increase in their ratio of insurance costs to total operating expenses between 16% and 20%, depending on location (Burbano, Holtermans, and Kok, 2025). On average, the ratio of insurance costs to total operating expenses has increased from 4.4% to 7%, with ratios as high as 20% in areas such as Florida or California.

Figure 1: Increasing burden for commercial real estate markets

Source: Burbano, Holtermans and Kok (2025) with NCREIF data

Economic losses and the protection gap

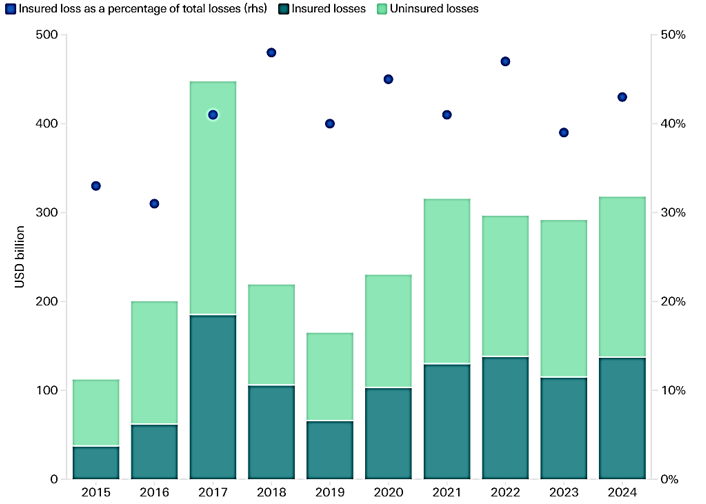

Global economic losses from natural disasters in 2024 reached USD 318 billion. Of this amount, only 43 percent, about USD 137 billion, was insured, leaving a substantial protection gap of roughly USD 181 billion. Overall, 2024 ranks among the costliest years on record in terms of insured losses (Munich Re). Looking ahead, insured losses are projected to remain elevated, reaching an estimated USD 145 billion in 2025 (Swiss Re).

The climate insurance protection gap is not merely an insurance problem; it has broader implications for fiscal sustainability and financial stability. Recent research highlights supply-side mechanisms that constrain coverage: (i) backward-looking risk assessment that underestimates non-linear, compounding hazards; in practice, this means that models based heavily on historical data fail to capture how small shifts in weather patterns can generate disproportionately large losses, or how multiple risks may occur together or in sequence; (ii) diversification is limited because catastrophic losses are often geographically concentrated, and extreme events can produce unexpectedly large payouts; (iii) liquidity constraints after large events; (iv) capital constraints due to regulation and solvency requirements. Demand-side factors also contribute to the protection gap. Insurance uptake depends on mandates, affordability, access to information, financial literacy, and individual risk perception. In addition, expectations of post-disaster public assistance can discourage property owners from purchasing coverage in advance, further widening the gap (Monasterolo, 2025).

Figure 2: Global natural catastrophe insured and uninsured losses, share of insured losses (USD bn, 2024 prices)

Source: Moody’s

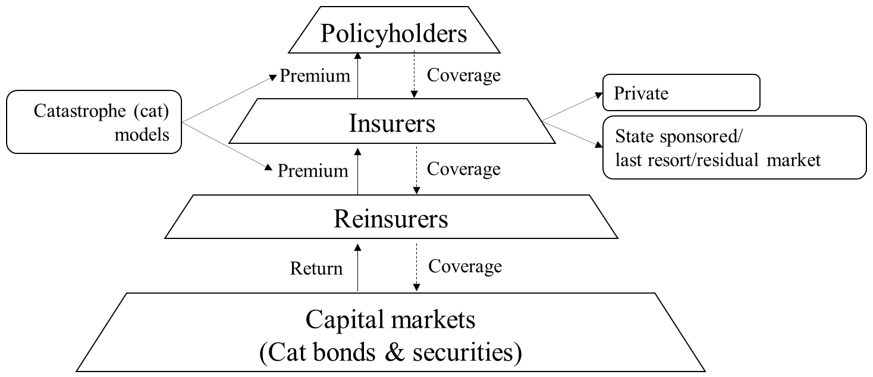

The existing insurance system is a layered pyramid

The property catastrophe risk ecosystem today can be conceptualized as a layered pyramid: households and firms purchase coverage from insurance companies, who, in turn, cover their risk through reinsurers and, increasingly, capital markets via catastrophe (CAT) bonds. In some countries, when private insurers are unable or unwilling to cover certain high-risk properties, government-backed programs step in as ‘insurers of last resort’ that provide coverage to the residual market for specific perils. In principle, prices and contract characteristics at each layer respond not only to expected losses but also to capital supply, regulatory design, and how insurers learn and adapt when risks are uncertain.

Figure 3: The insurance system as a layered pyramid

Source: Author based in Goda et al (2014)

The current public debate often focuses on the unexpected increase in premiums, but an equally important issue is whether coverage is still available in the first place. Availability refers not only to whether insurers are willing to offer a policy but also the conditions attached to it (capacity offered, deductibles, sublimits, and exclusions). Availability pressures become visible when private insurers withdraw from high-risk areas, forcing more people and businesses to rely on government-backed “last-resort” insurance programs. These programs help ensure that coverage remains accessible in the short run, but they also shift financial risk onto the government and taxpayers. Moreover, if prices in these programs do not reflect actual risk, they may reduce incentives for households, and firms to invest in gradual climate adaptations.

An emerging issue in insurance markets in the context of climate risk is cross-subsidization. Insurance companies with a presence in different geographical areas could raise the premiums in markets not affected by extreme weather events and with lighter regulatory restrictions to compensate for losses in areas highly exposed to natural disasters. This behavior can distort risk signals, and decouple prices from underlying hazards (Sen, 2024), thereby weakening the mapping from physical risk to observed premiums.

Reinsurance

Reinsurance acts as the release mechanism of the insurance pyramid, allowing losses from local disasters to be shared with global capital markets. After extreme natural catastrophes, reinsurance prices tend to rise, not only because the demand increases, but also because the supply of risk-bearing capital becomes more limited, reflecting greater caution among investors (Möhr, et al., 2025). Between 2017 and 2024, a series of severe catastrophe seasons led to repeated periods of higher reinsurance prices. These conditions then feed back to primary insurers, and ultimately, to policyholders. The result is a cyclical pass-through to buyers: higher deductibles, tighter policy terms, and insurers having to absorb more of the risk themselves after years with large losses (Froot, 1999; 2008).

Capital-markets capacity: CAT bonds and ILS

When traditional insurance and reinsurance capacity becomes constrained, insurers increasingly turn to catastrophe bonds (CAT bonds) and other insurance-linked securities (ILS) to transfer risk. These instruments operate differently from conventional reinsurance. Reinsurers rely on diversification and the strength of their ongoing business to manage risk efficiently, whereas CAT bonds are fully collateralized: the entire potential payout is funded upfront and held in a secure account. This structure reduces the risk that the counterparty cannot pay but requires considerably more capital. This design can improve the resilience of the insurance system by attracting new investors and expanding available risk-bearing capital. However, investors demand higher returns because they know there is a risk of trigger–loss mismatch (basis risk), a risk that a big disaster actually hits (event risk), and a risk that multiple bad events happen together in extreme seasons, making their overall portfolio more volatile (Lakdawalla & Zanjani, 2006).

Recent market data show that 2025 has seen record levels of new CAT bond issuance, with approximately USD 7.1 billion issued in the first quarter alone. Outstanding risk capital now exceeds USD 50 billion. While this growth reflects the increasing role of capital markets in absorbing catastrophe risk, the overall capacity remains modest relative to the size of the global protection gap.

Potential implications for commercial real estate investors

The property insurance system remains operational but is under increasing stress: premiums and deductibles are adjusting upward, contract terms are tightening, capacity is becoming more selective, and publicly backed insurance programs are playing a growing role in maintaining coverage. In the near term, the system’s resilience will depend on a steady flow of capital into reinsurance, catastrophe bonds, and other insurance-linked securities, as well as on public programs that price risk in a transparent and consistent way. Over the long run, continued uncertainty about the likelihood of very large, damaging events means that the cost of risk capital is likely to remain high, a pattern already visible in recent periods of severe losses and in the upward trend in both insured and uninsured damages. In this environment, the insurance system’s resilience will increasingly rely on reducing expected losses through effective adaptation measures.

For commercial real estate, this means higher and more unpredictable insurance costs, stricter policy conditions such as higher deductibles, and a greater risk that insurance may become hard to obtain in high-risk areas. Location and design choices matter: site-level adaptations (flood barriers, wind upgrades) improve underwriting outcomes and reduce expected losses. Investors may benefit from considering a range of strategies to manage rising insurance costs and coverage constraints associated with increased physical climate risks. To stabilize both coverage and pricing, multi-year insurance placements may become increasingly attractive. The market is also exploring parametric insurance layers (insurance policies that pay out automatically when specific, measurable parameters – such as rainfall, storm surge, or wind speed – reach a defined threshold, rather than compensating for actual losses) to help fill gaps created by exclusions or large deductibles. In addition, captives or reserve buffers can provide internal funding for post-event recovery when external insurance is limited or too expensive. Finally, investors could consider integrating forward-looking climate scenarios into acquisition and underwriting to avoid mispricing and to prioritize capital expenditures with quantifiable premium and loss-ratio paybacks.

Call upon other investors to collaborate to achieve real-world impact

GREEN is a not-for-profit collaborative engagement initiative for institutional investors, focusing on reducing climate risk in the real estate industry. GREEN members acknowledge the importance of collaboration to initiate change and maximize impact. We, therefore, call upon other institutional investors to join GREEN and work together towards a Paris-aligned real estate sector. Check the investor statement for more information.

Disclaimer

The views presented in this article reflect the views of the GREEN Secretariat but do not necessarily represent those of the individual GREEN members.

References

Burbano, P., Holtermans, R., & Kok, N. (2025). Climate risk and the insurability of commercial real estate. Mimeo.

Caisse Centrale de Réassurance (CCR). (2023). The consequences of climate change on the cost of natural catastrophes in France up to 2050.

Froot, K. A. (2001). The market for catastrophe risk: A clinical examination. Journal of Financial Economics, 60(2-3), 529-571.

Goda, K., Wenzel, F., & Daniell, J. (2015). Insurance and Reinsurance Models for Earthquake. DOI: 10.1007/978-3-642-35344-4_261.

Froot, K. A. & O’Connell, P. G. J. (1999). “The Pricing of U.S. Catastrophe Reinsurance,” NBER Chapters, in: The Financing of Catastrophe Risk, pages 195-232, National Bureau of Economic Research, Inc.

Lakdawalla, D., & Zanjani, G. (2006). Catastrophe bonds, reinsurance, and the optimal collateralization of risk transfer. NBER Working Paper No. 12742.

Shi, L., & Moser, S. (2021). Transformative climate adaptation in the United States: Trends and prospects. Science, 372

Möhr, C., Yong, J., & Zweimüller, M. (2025). Mind the climate-related protection gap – reinsurance pricing and underwriting considerations. FSI Insights on Policy Implementation No. 65.

Monasterolo, I. (2025). The climate insurance protection gap: Implications for financial stability and fiscal sustainability. SSRN Working Paper 5409046.

Moody’s. (2025). Catastrophic events in an uncertain future: A pending $41 trillion bill for businesses and governments to resolve.

Munich Re. (2025). Natural disaster figures 2024. Media Information.

Sen, I. (2024). Regulatory limits and cross-subsidization in property insurance markets. Harvard Business School Working Paper 24-077.

Shi, L., & Moser, S. (2021). Transformative climate adaptation in the United States. Science, 372(6549), 1278-1284.

Swiss Re Institute. (2025). Natural catastrophes in 2024. Sigma Research Report 2025-01.