Natural disasters pose a significant threat to real assets and the financial wealth of their owners. Recent examples include the Valencia floods in 2024 (causing around $18 billion in direct damages) and the LA wildfires in 2025 (causing around $31 billion in direct damages). However, direct damage is only part of the story. To understand how natural disasters affect real estate returns, it is important to realize that climate damage materializes through various channels. In this article, Philibert Weenink, PhD Candidate at the School of Business and Economics, Maastricht University, explores several mechanisms through which natural disasters can affect real estate returns at different geographic scales.

Direct Exposure: Physical Risk at the Property Level

The most obvious channel through which natural disasters affect financial returns is direct physical damage. However, since most buildings are insured, these damages typically materialize through higher insurance fees. This relation is well documented in academic literature, which shows that the rising frequency of natural disasters coincides with increasing insurance costs (Keys and Mulder, 2020). In some high-risk markets, insurers are even withdrawing altogether. Such constraints in insurance coverage limit investors in their risk management tools and reduce mortgage availability, as property insurance is typically required for obtaining a mortgage (see our previous GREEN article for details).

At the property level, owners also face the cost of adaptation measures. While these measures should pay off in the long run by mitigating risk and lowering both damages and insurance premiums, they do affect the timing of cash flows. Moreover, it remains unclear to what extent insurers adjust their fees in response to these property specific adaptation measures. The financial benefits of adaptation at the property level therefore remain uncertain.

Indirect Exposure: Economic Spillovers at the City Level

Beyond direct exposure, properties may also experience adverse outcomes more indirectly. Natural disasters can affect the demand for real estate by disrupting the local economy. Research shows that areas affected by natural disasters experience significant economic changes. For example, natural disasters can disrupt supply chains (Carvhalo et al. 2020), reduce household wealth (Belasen and Polachek, 2008), increase municipal bond yields (Goldsmith-Pinkham et al. 2023), hinder business growth (Addoum et al. 2023), and lead to rising out migration (Hornbeck, 2012).

The exact implications of these disruptions are difficult to generalize, as natural disasters differ in scale and impact. Moreover, some areas are more resilient than others. Kahn (2005), for example, shows that natural disasters in countries with high quality institutions result in fewer deaths than similar events in countries with low quality institutions. Despite this heterogeneity in exposure and resilience, the overall downside risk implications remain clear. By harming the regional economy, natural disasters can cause local businesses to go bankrupt, default on their lease contracts and ultimately reduce the demand for real estate (Glaeser and Gyourko, 2005).

Systematic Exposure: National Risk Transfer

At the national level, natural disasters may also impose systematic risk. In most countries, solidarity schemes exist to financially compensate victims of natural disasters. Effectively, this means that part of the risk is transferred from those with higher exposure to those with lower exposure. Cross-subsidies arise, for example, through insurance regulations that restrict premium differentiation (Oh et al. 2022) and through national disaster relief, which redistributes tax revenues to the affected regions (Botzen and Van den Bergh, 2008).

Moreover, central banks have raised concerns that extreme events may lead to macroeconomic and financial instability once they become sufficiently severe (Caloia and Jansen, 2021). As a result, even properties that are considered completely ‘safe’ may still experience adverse consequences of natural disasters.

Implications for Investors

While identifying direct property exposure to natural disasters is a critical first step in achieving financial resilience, it is important to recognize that damages may also materialize more indirectly. This implies that mitigation measures at the property level have their limits. To further enhance financial resilience, both direct and indirect risk exposure should be incorporated in price dynamics. In this regard, it is important to note that indirect exposure occurs at various spatial scales. This suggests that risk stemming from natural disasters has both idiosyncratic (property specific) and systematic components. Large scale adaptation measures and cross-country portfolio diversification are therefore needed to further mitigate risk.

Thus far, research has mainly focused on materialized price effects driven by direct exposure. To better understand price dynamics of properties that appear unexposed at first glance, more research is needed on the spill-over effects of natural disasters. Not only the spatial extent, but also the timing through which these indirect effects materialize, is relevant. It is encouraging that some investors already recognize the importance of indirect exposure. However, systematic approaches to incorporating this into portfolio strategy remain underdeveloped.

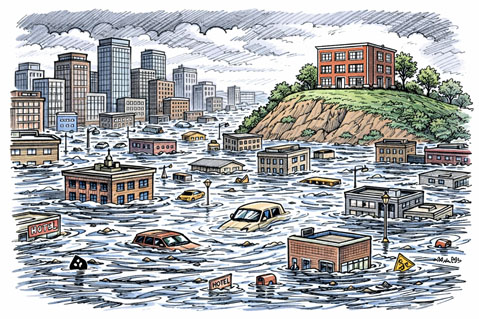

By fully understanding how natural disasters can affect local markets and even national economies, investors can incorporate this risk in their return requirements and consider strategies to diversify or mitigate them. Returning to the illustration above, while the building on the hill is clearly better off than others, it still faces the aftermath of the disaster. This raises an important question; how long will this property remain ‘prime real estate’ once all its surroundings are in decay?

Disclaimer

The views presented in this article reflect the views of the GREEN Secretariat but do not necessarily represent those of the individual GREEN members.

Literature

Addoum, J.M., Gounopoulos, D., Gustafson, M., Leis, R. & Nguyen, T. (2023). Does wildfire smoke choke local business to adapt? SSRN Working Paper, No. 4564296

Belasen, A. R., & Polachek, S. W. (2008). How Hurricanes Affect Wages and Employment in Local Labor Markets. American Economic Review, 98 (2), 49–53.

Botzen, W. J. W., & Van Den Bergh, J. C. J. M. (2008). Insurance against climate change and flooding in the Netherlands: Present, future, and comparison with other countries. Risk Analysis, 28(2), 413–426.

Caloia, F., & Jansen, D.-J. (2021). Flood risk and financial stability: Evidence from a stress test for the Netherlands. De Nederlandsche Bank Working Paper, No. 730.

Carvalho, V. M., Nirei, M., Saito, Y. U., & Tahbaz-Salehi, A. (2021). Supply Chain Disruptions: Evidence from the Great East Japan Earthquake. The Quarterly Journal of Economics, 136 (2), 1255–1321.

Glaeser, E.L. & Gyourko, J. (2005). Urban Decline and Durable Housing. Journal of Political Economy, 113(2), 345-375.

Goldsmith-Pinkham, P., Gustafson, M.T., Lewis, R.C., & Schwert, M. (2023) Sea-level rise exposure and municipal bond yields. The Review of Financial Studies, 36 (11), 4588-4635.

Hornbeck, R. (2012). The Enduring Impact of the American Dust Bowl: Short- and Long-Run Adjustments to Environmental Catastrophe. American Economic Review, 102 (4), 1477–1507.

Kahn, M.E. (2005). The Death Toll from Natural Disasters: The Role of Income, Geography, and Institutions. The Review of Economics and Statistics, 87(2), 271-284.

Keys, B., & Mulder, P. (2020). Neglected No More: Housing Markets, Mortgage Lending, and Sea Level Rise. NBER Working Paper, No. 27930.

Oh, S. S., Sen, I., & Tenekedjieva, A.-M. K. (2022). Pricing of climate risk insurance: Regulation and cross-subsidies. FEDS Working Paper, No. 2022-64.