Rising Risks, Soaring Costs: How reinsurance markets are influencing home insurance premiums

Insurance companies purchase reinsurance to manage the growing number of significant and catastrophic claims caused by climate events. Reinsurance allows insurers to transfer some of their concentrated risks, reducing the financial impact of claims that exceed certain thresholds. While previous studies have explored the relationship between climate change and insurance premiums, none have specifically examined how reinsurance markets are affecting housing insurance premiums within the context of climate change.

Alexander Carlo, a Doctoral Candidate in Finance at Maastricht University’s School of Business and Economics, examines recent research revealing a substantial increase in homeowners’ insurance premiums, particularly in disaster-prone areas. Notably, this study is the first to investigate the influence of reinsurance markets on these premiums, offering unprecedented insights into how global capital flows impact local real estate dynamics.

Rising Insurance Costs U.S. Hit High-Risk Areas Hardest: 33% increase in 3 years

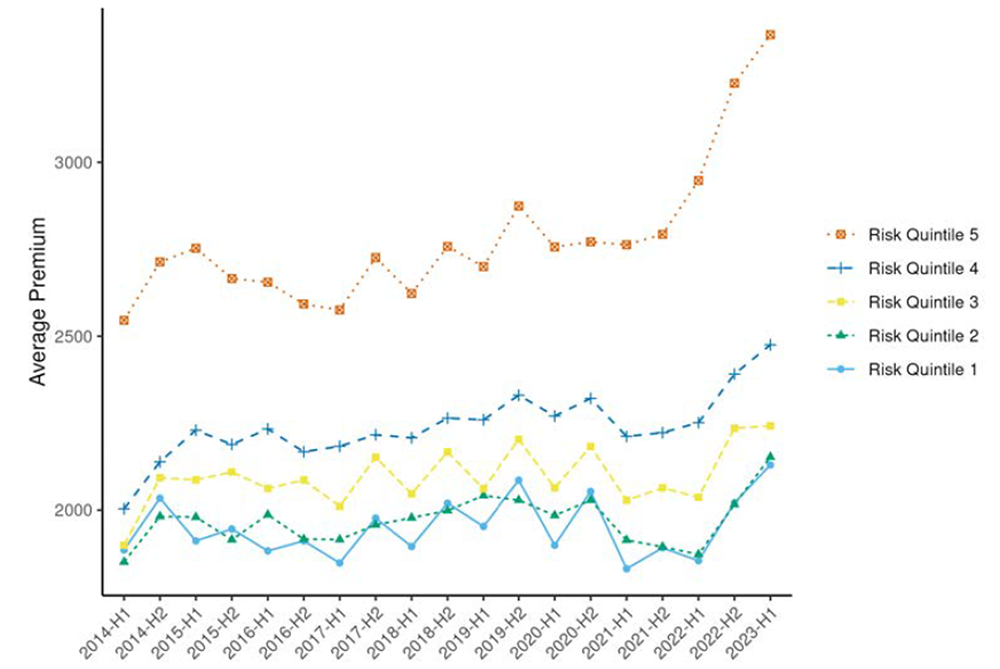

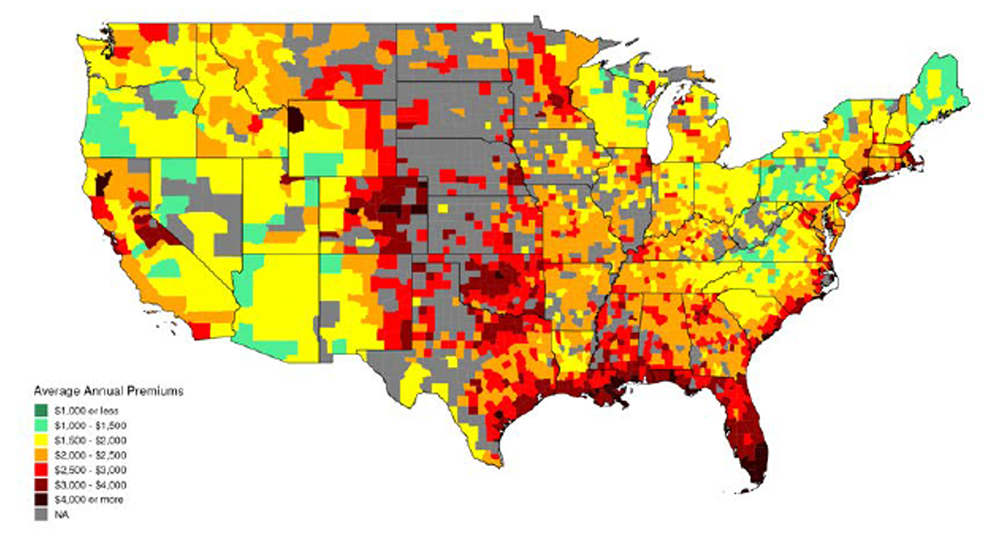

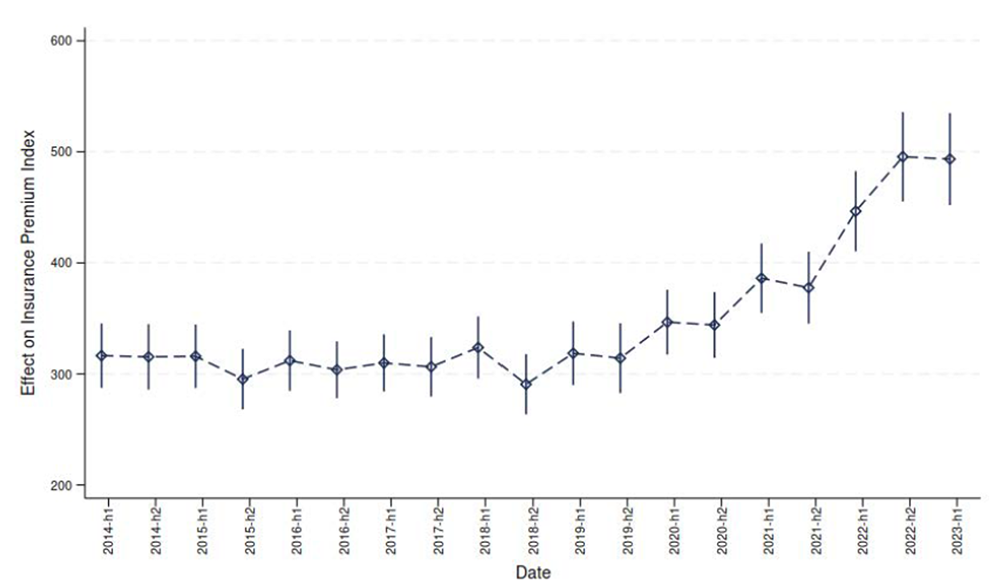

A comprehensive study published by the National Bureau of Economic Research analysed 47 million data points from 2014 to 2023, finding that U.S. homeowners’ insurance costs have risen significantly, with the most dramatic increases occurring in high-risk areas (see Figure 1). The study shows that average annual premiums surged by 33%, rising from $1,902 in 2020 to $2,530 in 2023—an increase of 13% in real terms. Coastal regions prone to natural disasters, such as the Gulf of Mexico and the East Coast, and tornado- and flood-prone areas of Oklahoma and North Texas, had the highest premiums in the first half of 2023 (see Figure 2). The research showed that a one standard deviation increase in disaster risk correlates with an average annual premium of $335. Moreover, this impact has increased over time, with the premium increase linked to the same risk rising from $300 in 2020 to nearly $500 in 2023 (see Figure 3).

Figure 1 shows average premiums in 2023 dollar prices plotted by quintile of disaster risk exposure. The first quintile includes the 20% of the population with the lowest disaster risk, the second quintile the next 20%, and so on, up to the fifth quintile, which includes the 20% with the highest risk.

Figure 2 maps the average annual insurance premiums by county in the first half of 2023.

Figure 3 plots the time-varying estimated effect of disaster risk on premiums. Vertical lines indicate 95% confidence intervals.

Reinsurance Price: A 100% increase in the last decade

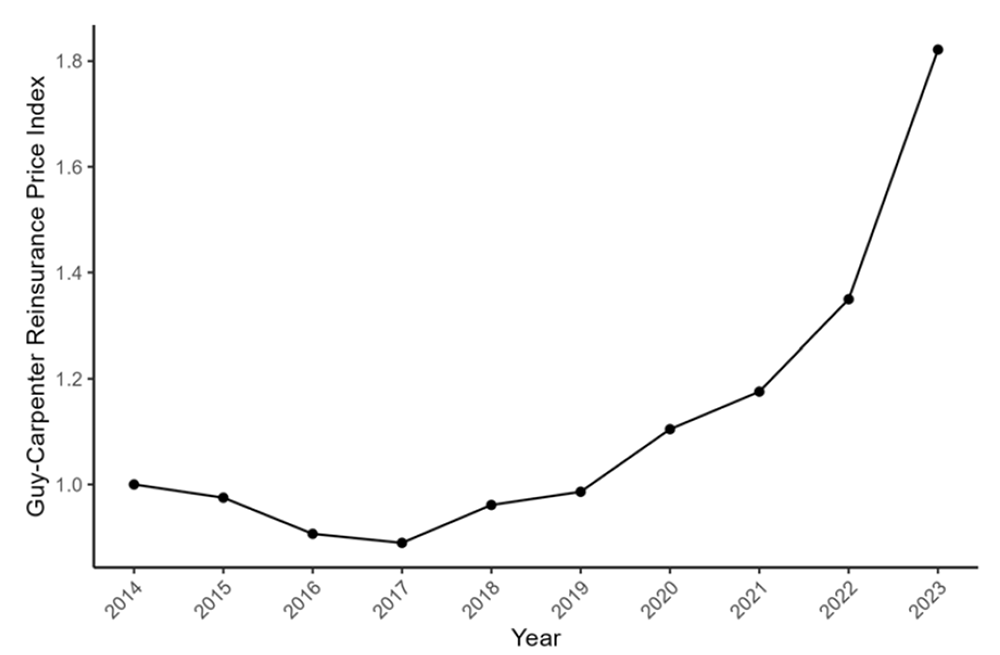

Disaster risk started to have a more significant effect on insurance premiums (Figure 3) at the same time that U.S. property catastrophe reinsurance prices doubled between 2018 and 2023. Reinsurance involves secondary insurance contracts with global insurers that U.S. insurers use to manage correlated or severe risks, such as those posed by hurricanes and wildfires. The Guy-Carpenter U.S. Property Catastrophe Rate-on-Line Index measures reinsurance prices (Figure 4), which approximately doubled from 2014 to 2023.

Thus, insurance pricing offers valuable insight into the cost of covering risks projected to rise due to climate change. The doubling of reinsurance prices can likely be attributed to increased exposure to disaster risk due to population shifts into vulnerable areas and the end of the low-interest-rate period, which led to a capital squeeze and inflation. It also reflects a change in reinsurers’ perception of climate risks. This raises the question of whether reinsurers adjust prices in response to the same factors driving up premiums across the U.S. or if insuring against catastrophic risks is becoming uniquely expensive.

Figure 4 plots the time series of the Guy-Carpenter U.S. Property Catastrophe Rate-on-Line Index.

Reinsurance Price: A key driver of Rising Insurance Premiums

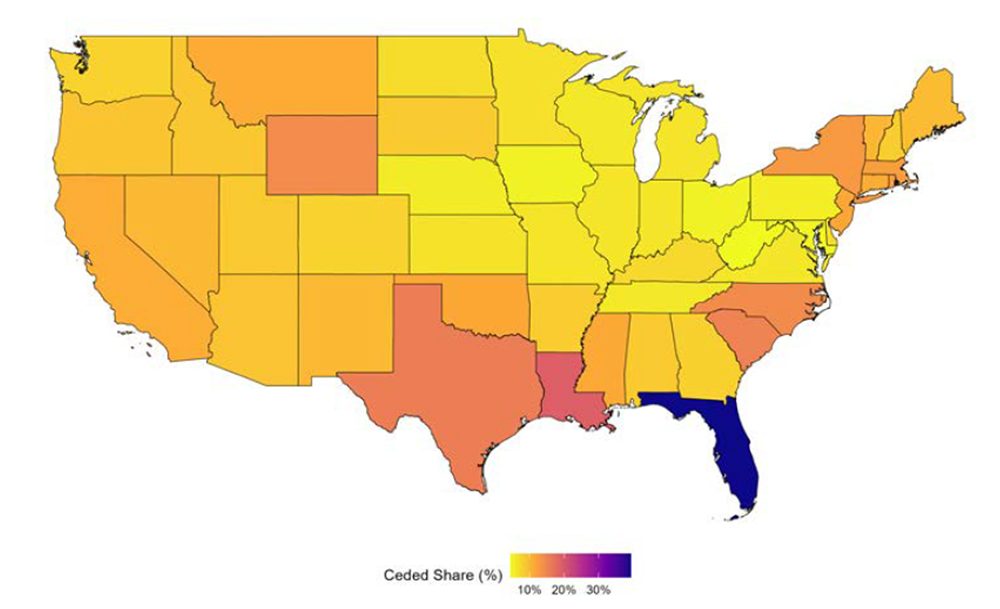

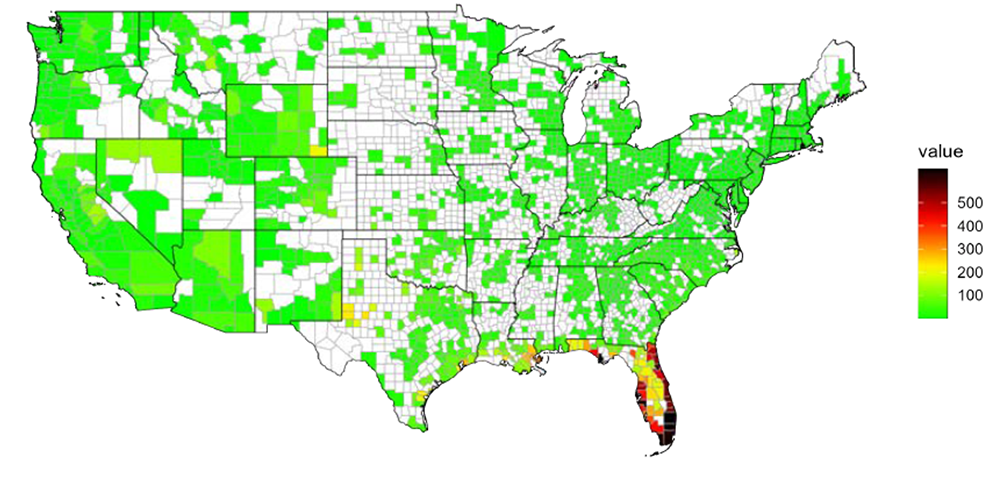

Figure 5 highlights that reinsurance exposure is highest in states with more significant disaster risks, such as hurricane-prone Florida, which aligns with reinsurance’s primary role in managing catastrophe risk. The study finds that reinsurance exposure explains nearly two-thirds of the increase in the impact of disaster risk on insurance premiums. Figure 6 illustrates that this effect is particularly pronounced in disaster-prone areas such as Florida, with the reinsurance shock adding an average of $375 to annual premiums for households in the top 10% of disaster risk by 2023.

Figure 5 maps state-level reinsurance exposure. Reinsurance exposure for each state is defined as the market-share weighted average of the share of premiums ceded by each insurer.

Figure 6 plots reinsurance shocks by county. Reinsurance shocks are calculated as the actual dollar increase in premiums between 2018 and 2023 caused by rising reinsurance prices.

Implications for Homeowners: Another increase of $700 per year in the next 30 years

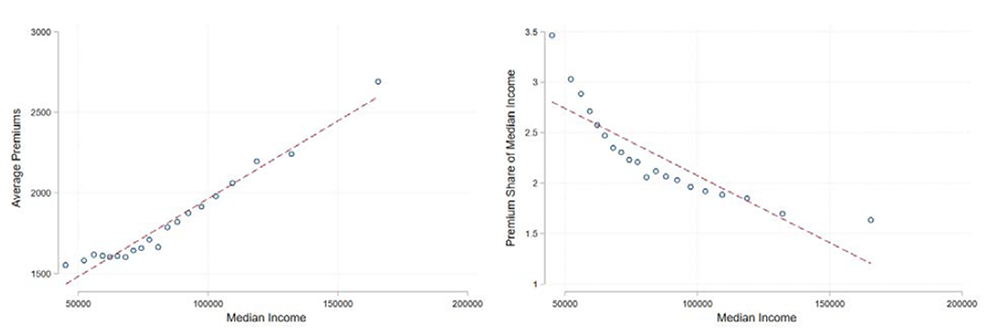

As the real estate industry grapples with climate change, this study highlights the growing financial burden of disaster risk on homeowners and the pivotal role that reinsurance markets play in this dynamic. Homeowners are expected to bear a higher insurance burden in the future (see Figure 7). This burden will be particularly severe for lower-income households (right panel of Figure 7). The estimates provided in this study represent a lower-bound estimate, i.e., the best-case scenario, assuming individuals can still obtain home insurance. Some insurance companies have recently stopped issuing policies in high-risk areas.

Looking ahead, the study projects that if current trends continue, homeowners in the most climate-exposed areas could see their insurance premiums increase by an additional $700 per year by 2053.

Figure 7 shows average premiums (left panel) and average premiums as a share of income. (right panel) by twenty ventiles of zipcode median income. Income is the median income of owner-occupied households from the 2014–2018 American Community Survey measured in 2018 dollars. Average premiums are taken over 2014–2018 and measured in 2018 dollars.

Implications for Commercial Real Estate Investors

These findings are also relevant to institutional investor’s commercial real estate investments. Lenders typically require that properties be insured for commercial real estate loans. As insurance companies pass through higher reinsurance rates to borrowers, similar to what we currently see in the housing market, commercial real estate valuations may decline. Institutional investors will increasingly need to consider increases in insurance costs when adding properties to their portfolios, especially those in higher-risk areas.

Call upon investors to collaborate and achieve real-world impact

GREEN is a not-for-profit collaborative engagement initiative for institutional investors, focusing on reducing climate risk in the real estate industry. GREEN members acknowledge the importance of collaboration to initiate change and maximize impact. We, therefore, call upon other institutional investors to join GREEN and work together towards a Paris-aligned real estate sector. Check the investor statement for more information.

Disclaimer

The views presented in this article reflect the views of the GREEN Secretariat but do not necessarily represent those of the individual GREEN members.