Understanding the Impact of Climate Risk on Real Estate Valuations

The increasing frequency and intensity of climate-related events, such as coastal flooding, rising sea levels, wildfires, land subsidence, and heat waves, pose significant risks to real estate markets worldwide. Climate-related events can cause physical damage to properties, and chronic climate risks such as rising sea levels and erosion threaten the long-term viability of properties in coastal locations, reducing their value over time.

In this blog, Niu Dongxiao, Postdoctoral Researcher at Maastricht University School of Business and Economics, explores the evidence of variations in valuation in high-risk zones, the importance of incorporating mitigation measures like climate risk and adaptation strategies into real estate valuations.

Properties exposed to climate events experience discount in value from 2% to 20%

Numerous academic studies have analyzed differences in property values, mortgage performance, and lender behaviour in high-risk areas. The value of properties in regions exposed to extreme climate events can have a discount of between 2%-20% compared to that of similar properties in less risky areas. A recent paper published in Nature Climate Change states that residential properties in the US exposed to higher flood risk are overvalued by US$121-237 billion, with the overvaluation varying across regions. This overvaluation occurs because these properties do not properly factor in the costs of future damages. Highly overvalued homes are concentrated in areas with little flood risk regulation and climate risk perceptions.

For the Netherlands, Bosker et al. (2019) found that all else equal, house prices are on average 1% lower in places that are at risk of flooding, which seems to be a small discount compared to the US evidence. For one, the frequency of catastrophic flooding events is much lower in the Netherlands. For another, flood risk information disclosure is not well regulated in the process of housing transactions, so market participants have a lower flood risk perception. The authors also state that for commercial buyers, which should be more risk-aware, the price penalty is larger. In the commercial real estate market, both Addoum et al. (2021) and Holtermans et al. (2022) examine the impact of hurricanes on property values and discover that commercial properties at risk of flooding trade at a considerable discount following a hurricane.

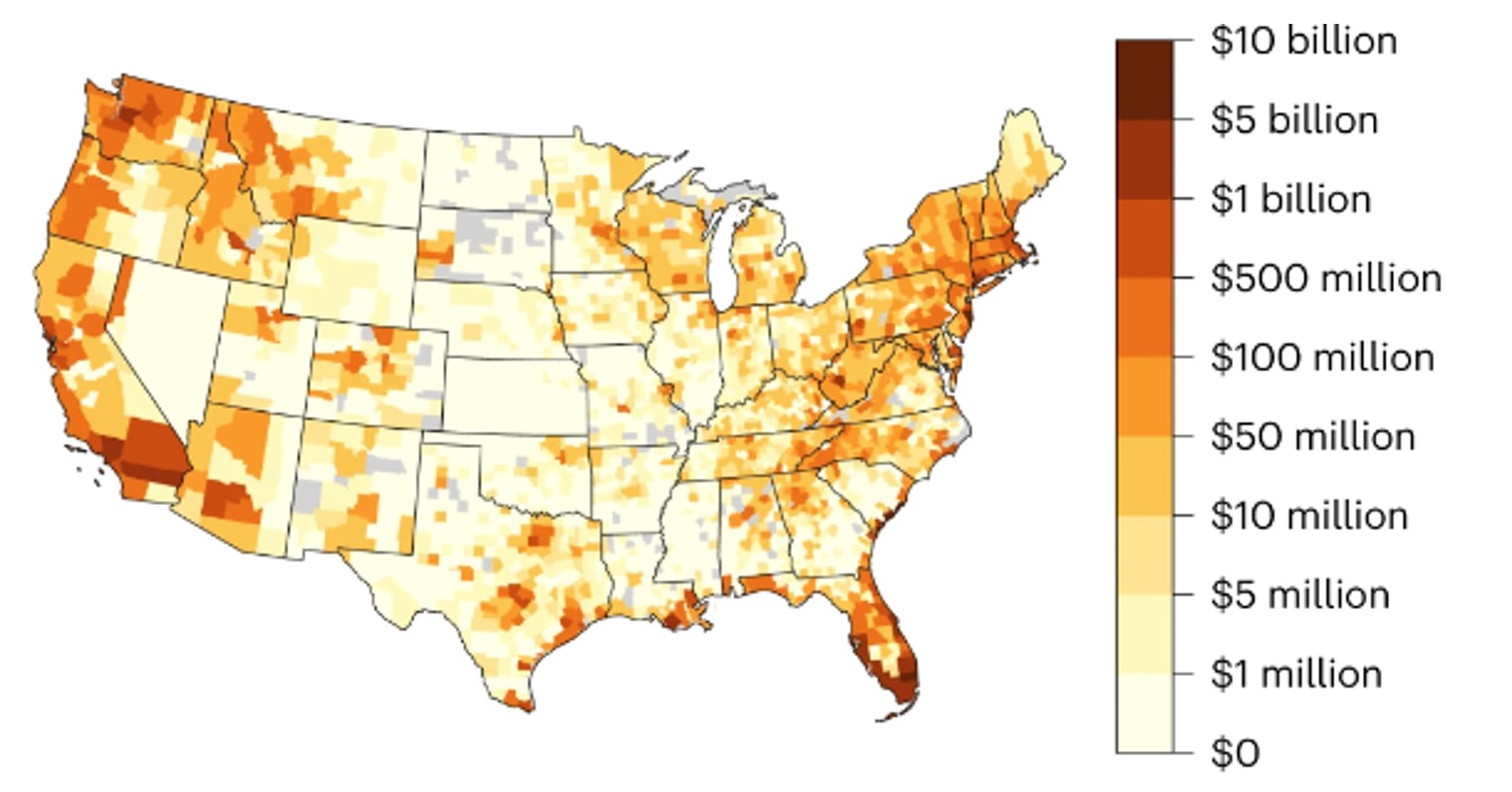

Figure 1. Climate risk and total overvaluation in dollars in the US

Notes: Figure from Gourevitch et al. (2023).

Perceptions of physical risk also affect the behaviour of lenders

Apart from the transaction market, the decrease in home values may lead to changes in mortgage lenders’ perception and behavior, which will have direct consequences for real estate financing. Research finds that mortgage defaults and insurance premiums tend to be higher in high-risk zones (Issler et al., 2019; Kousky et al., 2020), reflecting the increased risks associated with owning property in these areas. In order to transfer climate risk, lenders are also more likely to approve mortgages that can be securitized (Ouazad and Kahn, 2021).

Factoring in Mitigation Measures to Reflect Net Physical Risk

Given the continuing process of climate change and the likelihood of climate shocks in vulnerable areas, it is essential to incorporate adaptation and mitigation strategies. California has also implemented strict earthquake and wildfire prevention measures, such as creating defensible space around properties, to mitigate the risk of property loss. The California Residential Mitigation Program provides grants to renovate homes not built to risk-resistant codes.

Newly-built homes in those areas previously affected by wildfire damage are actually more valuable than typical existing homes because the local government imposes new building codes and the newly-built homes are of higher quality (Issler et al., 2020). Mitigation measures such as structural elevation in Miami and New York resulted in the house price appreciation of approximately 11%-15% (Kim, 2020). Similarly, levee-protected commercial properties sell for approximately 8% more than similar properties in 100-year floodplains without protection (Fell and Kousky, 2015).

Despite high climate risk, many new homes are still constructed in the path of hurricanes or wildfires, because of their water view or forest view. The lack of regulation preventing building in the most hazardous area poses risks to homeowners, investors, and insurers, but adaptation and mitigation measures can mediate the magnitude and distribution of climate-related costs. However, there remain challenges in quantifying and incorporating these adaptation and mitigation measures into property valuations, such as determining the effectiveness of different adaptation strategies and accounting for uncertainties in future climate impacts.

Conclusion: proactive approach helps to maximize long-term gains

Generally, anecdotal and academic evidence suggests that climate-related events or physical risks lead to a price discount for both commercial and residential properties in certain areas, with the potential to affect property values and returns on investment. The availability of finance is also negatively affected in high-risk areas. Furthermore, these effects might be short-lived or long-lived, depending on local market economies, government intervention, and insurance. Investors’ sophistication and risk-related information provision both play a critical role in risk salience. By staying ahead of the curve and adopting a proactive approach to pricing in physical risks, savvy investors can better navigate this shifting landscape and maximize their long-term gains in a rapidly evolving market.

Large room for further research on how to better reflect net physical risks

Undoubtedly, this is a new and evolving area of research that needs more granular and accurate data to allow more precise assessments of property values that factor in climate risk exposure. One aspect that warrants further exploration is the balance between incorporating climate risk into property values and government interventions to mitigate property owner risks. Factoring in potential climate risk costs could adversely impact homeowners’ wealth, given that housing assets make up a significant portion of household wealth and contribute to local government tax revenue. On the other hand, if the government intervenes by buying out all properties in risky areas or building flood defenses, such investment has the potential to incentivize further development in flood-prone regions.

Call upon other investors to collaborate to achieve real-world impact

GREEN is a not-for-profit collaborative engagement initiative for institutional investors, focusing on reducing climate risk in the real estate industry. GREEN members acknowledge the importance of collaboration to initiate change and maximize impact. We, therefore, call upon other institutional investors to join GREEN and work together towards a Paris-aligned real estate sector. Check the website of GREEN for more information.

Disclaimer

The views presented in this article reflect the views of the GREEN Secretariat but do not necessarily represent those of the individual GREEN members.

Reference:

- Addoum, J. M., Eichholtz, P., Steiner, E., & Yönder, E. (2021). Climate change and commercial real estate: Evidence from hurricane sandy. Available at SSRN 3206257.

- Bosker, M., Garretsen, H., Marlet, G., & van Woerkens, C. (2019). Nether Lands: Evidence on the price and perception of rare natural disasters. Journal of the European Economic Association, 17(2), 413-453.

- Fell, H., & Kousky, C. (2015). The value of levee protection to commercial properties. Ecological Economics, 119, 181-188.

- Gourevitch, J. D., Kousky, C., Liao, Y., Nolte, C., Pollack, A. B., Porter, J. R., & Weill, J. A. (2023). Unpriced climate risk and the potential consequences of overvaluation in US housing markets. Nature Climate Change, 1-8.

- Hino, M., & Burke, M. (2021). The effect of information about climate risk on property values. Proceedings of the National Academy of Sciences, 118(17), e2003374118.

- Holtermans, R., Niu, D., & Zheng, S. (2022). Quantifying the Impacts of Climate Shocks in Commercial Real Estate Market. Available at SSRN 4276452.

- Issler, P., Stanton, R., Vergara-Alert, C., & Wallace, N. (2020). Mortgage markets with climate-change risk: Evidence from wildfires in California. Available at SSRN 3511843.

- Kim, S. K. (2020). The economic effects of climate change adaptation measures: Evidence from Miami-Dade County and New York City. Sustainability, 12(3), 1097.

- Kousky, C., Palim, M., & Pan, Y. (2020). Flood damage and mortgage credit risk: A case study of Hurricane Harvey. Journal of Housing Research, 29(sup1), S86-S120.