The cost of climate risk in U.S. real estate markets: The role of insurers

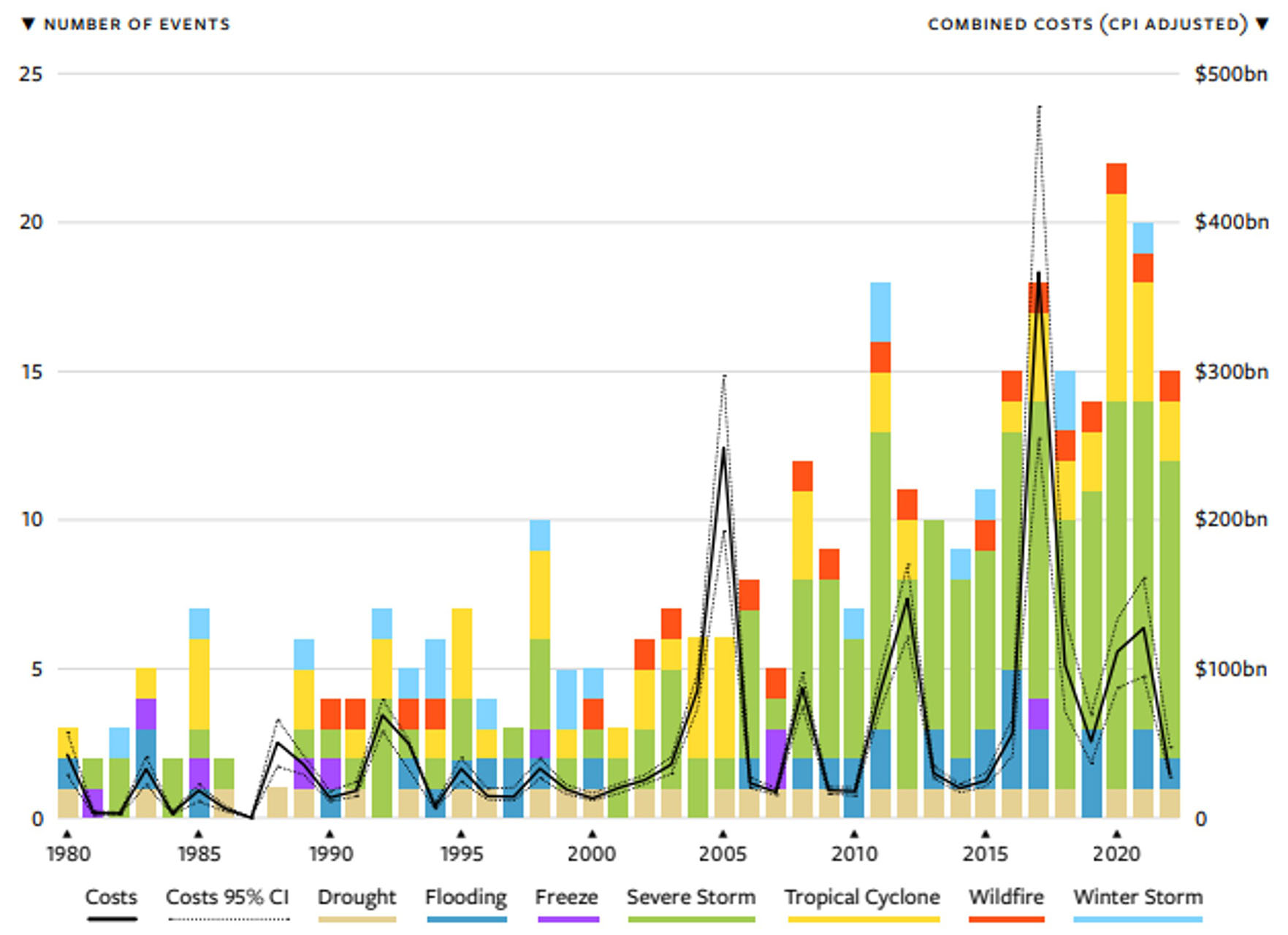

The economic costs of large natural disasters, as measured by the National Oceanic and Atmospheric Administration (NOAA), have grown steadily over recent decades. In the last 10 years, these large disasters cost the U.S. at least $1 trillion in total (see Figure 1)[1]. Private real asset owners claim to protect themselves against these economic losses by buying insurance policies. Insurance markets however are not a panacea for the impacts of climate change and at some point, policies could become unaffordable, while some insurers are already exiting high-risk markets. Alexander Carlo, Doctoral Candidate in Real Estate Finance at the School of Business and Economics, Maastricht University, explores some potential consequences.

Increasing costs of natural disasters in the US

The two most common examples are flood- and wildfire insurance. Given the increased incidence of climate disasters, will insurance markets have an increasing influence on how climate change affects real estate assets’ risk/return profile?

Figure 1. Cost and Frequency of U.S. Billion-Dollar Climate Disasters

Data source: NOAA National Center for Environmental Information.

Note: Costs are a summary of government expenditures, insurance claims, and economic losses. For more detail, see https://www.ncei.noaa.gov/access/billions.

Dwindling coverage of flood and wildfire insurance in high risk markets

In contrast to damage caused by fire and smoke, flood damage is excluded from the standard homeowners and renters insurance policies[2]. However, flood coverage is available separately from the National Flood Insurance Program (NFIP), administered by the Federal Emergency Management Agency (FEMA), and from several private insurers.

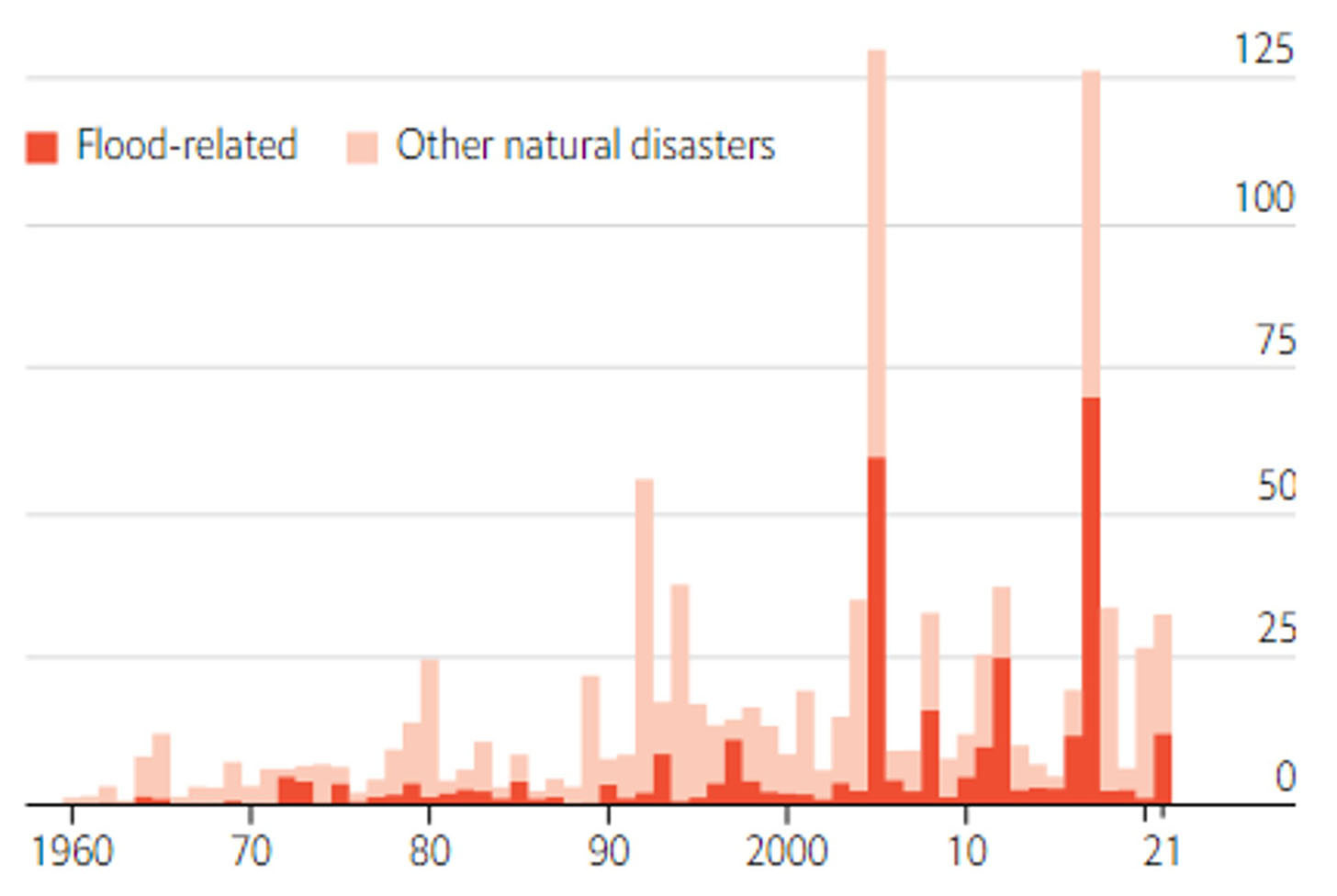

According to the Federal Emergency Management Agency (FEMA), there are approximately 5 million flood-risk policyholders in the country. Furthermore, the National Flood Insurance Program provides nearly $1.3 trillion in coverage against flooding, making it the US’s largest-single line insurance program. This is unsurprising as floods are America’s most expensive type of natural disaster, causing at least $323bn in direct damage since 1960 after accounting for inflation (see Figure 2[3]).

Figure 2 Direct property damage, $bn

California was the state with the largest number of properties at high to extreme risk from wildfires, in 2021. According to data from the California Department of Insurance, there are approximately 9 million wildfire risk-policy holders. More specifically, the California FAIR plan covers residential and commercial properties located in brush and wildfire areas at higher rates due to the increased risk of fire. However, the amount of policies that are not renewed or canceled has been steadily increasing over the past 5 years[4].

Regulatory intervention hampers the function of markets

As disastrous climate events become more commonplace, it is becoming apparent that the regulatory interventions imposed by politicians to keep policy premiums affordable are pushing insurers away.

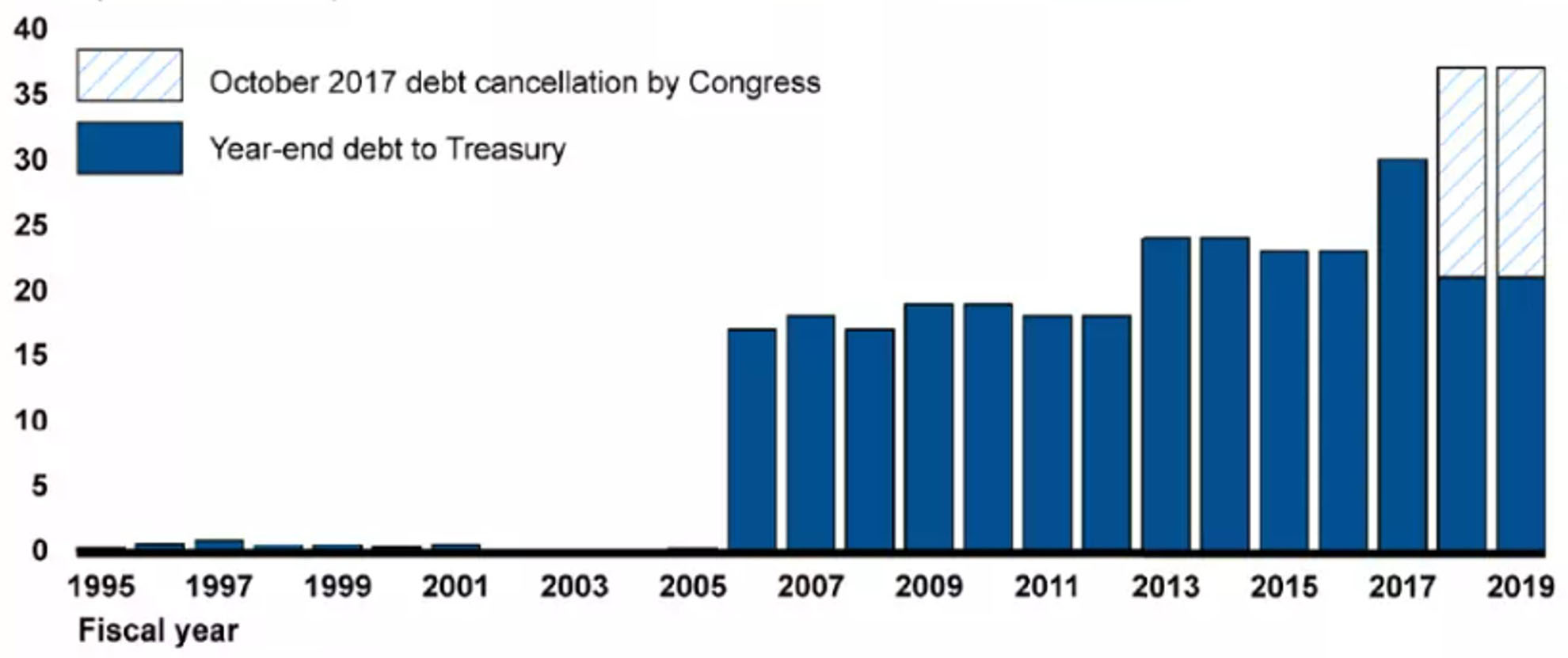

For the National Flood Insurance Program, the growing magnitude of major flood events and the historical focus on keeping homeowners’ and commercial policy rates affordable have come at the expense of the program’s solvency. Specifically, the U.S. Congress has historically required the program to charge discounted premium rates to ensure affordability, which resulted in the NFIP borrowing approximately $37 billion from Treasury since 2005[5] (see Figure 3). In 2022, the NFIP owed $20.5 billion to the Treasury.

Figure 3 National Food Insurance Program Annual Year-end Debt to Treasury, Fiscal Years 1995-2019 Debt (dollars in billions)

Source: GAO analysis of Treasury data. | GAO-20-508

Consequently, many insurers are not issuing new policies in the state of Florida, leaving the market to a handful of players that are also struggling to stay solvent. This is despite the state’s average annual property insurance payment being nearly triple the national rate ($4,231 versus $1,544), according to the Insurance Information Institute, an industry association[6].

On the West coast, there is a growing number of wildfire risk insurers leaving the market. State Farm and Allstate Corp., two of the biggest insurers in California, both stopped accepting new policy applications for property insurance. According to data from the California Department of Insurance, approximately 13% of homeowners and dwelling fire policies were not renewed by insurance companies in 2021. This is mainly due to policies requiring insurers to set policy rates for annual catastrophic coverage as a fraction of damages accrued over 20 years — without mention of models that can capture the increased likelihood of climate change[7].

Policy: different scenarios for the insurance market

The impact of extreme weather events on the insurance market could result in several potentially negative outcomes. Regulators could maintain the current approach of imposing policy rate caps. The effect will be that more insurers withdraw from specific markets, making it impossible for owners to insure their properties and may even prevent them from securing finance.

Alternatively, policymakers could remove policy rate caps, resulting in significant increases in insurance premiums. To avoid making climate risk policies unaffordable, driving residents and investors out of those markets, the policy rates can be reduced to reward home and business owners for implementing mitigation efforts.

For example, California passed a law in 2022 that requires insurers to reward home and business owners for their fire mitigation efforts. However, this is precisely the reason why some insurance companies leave the market. Namely, if they have to give discounts on top of policy rates that are already capped, it is not financially viable for the insurers anymore. Is it time the government let insurance premiums genuinely reflect the true level of climate risks?

Insurers cannot protect real estate from the growing threat of extreme weather events

The challenges that homeowners and insurers are facing on both coasts of the US illustrate the limitations of insurance against the effects of climate change. Insurance is not a panacea for climate risk protection, rather it is a complement to investing in mitigation and adaptation measures. Moreover, in the absence of mitigation, there is a real risk that certain markets will become uninsurable and ultimately uninvestable in the future.

Call upon other investors to collaborate to achieve real-world impact

GREEN is a not-for-profit collaborative engagement initiative for institutional investors, focusing on reducing climate risk in the real estate industry. GREEN members acknowledge the importance of collaboration to initiate change and maximize impact. We, therefore, call upon other institutional investors to join GREEN and work together towards a Paris-aligned real estate sector. Check the investor statement for more information.

[1] https://blogs.edf.org/markets/wp-content/blogs.dir/32/files/2023/01/Inclusive-Insurance-Report.pdf

[2] https://www.iii.org/fact-statistic/facts-statistics-flood-insurance

[3] https://www.economist.com/graphic-detail/2023/04/25/accounting-for-flood-risk-would-lower-american-house-prices-by-187bn

[4] https://www.insurance.ca.gov/01-consumers/200-wrr/upload/CDI-Fact-Sheet-Residential-Insurance-Market-Policy-Count-Data-December-2022.pdf

[5] https://www.gao.gov/blog/wave-concerns-facing-national-flood-insurance-program

[6] https://www.bloomberg.com/news/articles/2023-05-23/five-ways-hurricanes-make-hurricanes-more-expensive-in-florida

[7] https://casetext.com/regulation/california-code-of-regulations/title-10-investment/chapter-5-insurance-commissioner/subchapter-48-review-of-rates/article-4-determination-of-reasonable-rates/section-26445-catastrophe-adjustment