Focused collaborative engagements can deliver meaningful reductions in the intensity of CO2 emissions

What is the impact of investors’ engagement efforts? What makes engagements successful? Do engagements lead to positive cumulative excess returns? Alexander Carlo, Doctoral Candidate at Finance, School of Business and Economics, Maastricht University, elaborates it in this article.

The impact of investors’ engagements efforts

Increasingly institutional investors are engaging with companies in their portfolios about ESG issues. Moreover, when they engage, they are more likely to do so privately than to file a shareholder proposal. These private engagements (i.e., letters, calls, and meetings) are important because regulation limits the depth of shareholder proposals (i.e., filing and voting on shareholder proposals). On the other hand, these engagements use significantly more time and resources compared to exclusion-based investment strategies.

Yet, despite their increased importance, there is little academic evidence of the success of investors’ engagement efforts on target firms. What are the determinants of a successful engagement, and consequently, what are the effects on the target firms’ financial and ESG performance? A recent study conducted by Maastricht University fills this gap, providing insights into the consequences of private engagement efforts on target firms’ financial and ESG performance. The answer leans to a “Yes.” Successful engagements lead to excess returns and improved ESG performance.

What makes engagements successful?

In their study, the authors looked at approximately 7500 private engagements from 2007 to 2020 based on data from the asset manager Columbia Threadneedle Investments UK International Limited. They found that over their entire sample, approximately 20% of the engagement efforts culminated in an achieved milestone, and could be deemed successful. Given that 80% of the engagements do not achieve a milestone, it is crucial to understand the determinants of a successful engagement sequence.

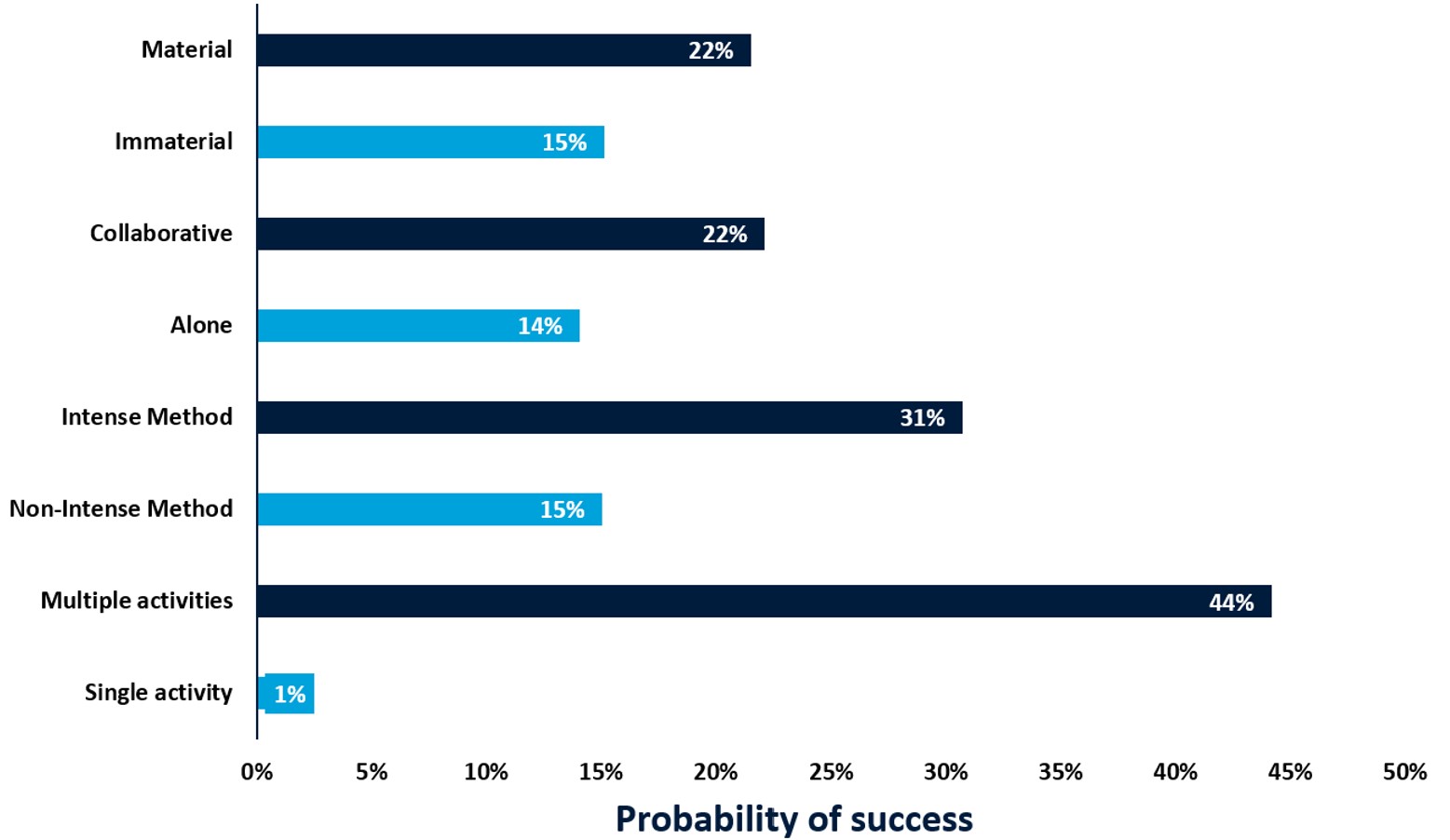

The authors conclude that four key factors improve the success rate of engagements (see Figure 1). The findings suggest that a one-size-fits-all engagement strategy is less effective and that financial materiality should be at the forefront of the engagement process. Most notably, multiple contacts between the investors and the target firm also increase the likelihood of reaching a milestone. Furthermore, the success rate increases when investors collaborate and use more intense engagement methods (e.g., calls or physical meetings vs. emails or letters). In addition, collaboration allows investors to share the costs with each other. In addition, the success rate of engagements increased when materiality was prominent in investor engagements. This can be achieved by using the Sustainability Accounting Standards Board (SASB) and MSCI Standards as a framework. For example, climate resiliency measures are important to real estate assets and funds but might not be as relevant for a company in the transport sector.

Figure 1: The four key factors improving the success rate of engagements

Engagements lead to positive cumulative excess returns

Interestingly, the authors find positive and significant outperformance following material engagements, regardless of whether the engagements have a recorded milestone or not. Overall, they find that firms targeted by successful material engagements significantly outperform peers by 2.5% over the following 14 months (i.e., the median time it takes to reach success). This result also holds when looking at the environmental category separately, where they find that the average cumulative risk-and peer-adjusted abnormal returns in the 14 months after a material engagement are 2.4%, whilst abnormal returns of immaterial engagements are not statistically significant. This highlights the importance of making financial materiality salient in engagement efforts.

ESG performance

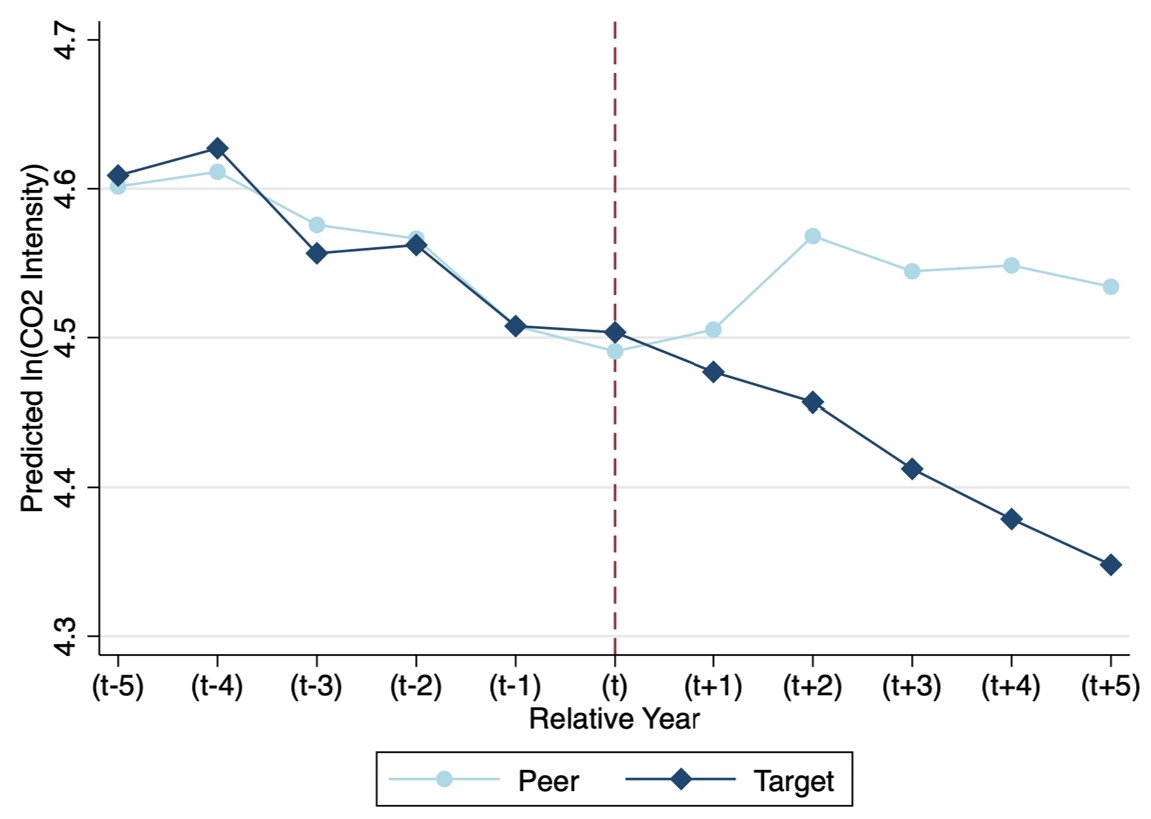

The authors also find significant improvements in the MSCI ESG score and the environmental score of target firms. For example, they find a 3.4% increase in target firms’ MSCI Environmental score in the years after being targeted. Next to the ESG scores, the engagement efforts lead to a 12.4% decrease in CO2e intensity (scope 1 and 2 emissions divided by sales) after the engagement, relative to peers (Figure 2). This effect is stronger when the engagement specifically addresses corporate emissions (-24.6%).

Figure 2

Implications for engagements in the real estate sector

The implications of this study are crucial for real estate investors, highlighting the importance of putting financial materiality at the core of engagement efforts. The real estate sector is responsible for 40% of all global carbon emissions and is one of the sectors most exposed to the negative consequences of climate change. The research findings suggest that engagement efforts focused on the environmental component of ESG can deliver material benefits. Additionally, collaboration with others and multiple engagements increase the likelihood of achieving milestones and lowering investors’ costs.

Finally, the study concludes that engagement efforts can lead to reductions in CO2e intensity after an engagement and especially when engagements specifically address corporate emissions.

Call upon other investors to collaborate to achieve real-world impact

GREEN is a not-for-profit collaborative engagement initiative for institutional investors, focusing on reducing climate risk in the real estate industry. GREEN members acknowledge the importance of collaboration to initiate change and maximize impact. We, therefore, call upon other institutional investors to join GREEN and work together towards a Paris-aligned real estate sector. Check the website of GREEN for more information.

Disclaimer

The views presented in this article reflect the views of the GREEN Secretariat but do not necessarily represent those of the individual GREEN members.

References

Bauer, R., Derwall, J., & Tissen, C., (2022). Private Shareholder Engagements on Material ESG Issues. Available at SSRN: https://ssrn.com/abstract=4171496 or http://dx.doi.org/10.2139/ssrn.4171496

Carlo, A., Eichholtz, P., & Kok, N. (2021). Three Decades of Global Institutional Investment in Commercial Real Estate. Journal of Portfolio Management, 47(10), 25-40. https://doi.org/10.3905/jpm.2021.1.275