Decarbonisation in a changing real estate investment landscape

Institutional investors have significantly increased their allocation to real estate in recent decades, accompanied by a move from traditional property types like offices to data centers, storage, and healthcare facilities. Real estate accounts for approximately 40% of global CO2 emissions, of which 70% comes from operational energy use. This raises an important question: How can the sector reconcile the drive toward net-zero ambitions with the rising prominence of energy-intensive property types like data centers in investment portfolios?

In this article, Alexander Carlo, a Ph.D. candidate at Maastricht University, examines how this shift in portfolio composition will impact real estate investors’ ambitions to reduce CO2, while highlighting gaps in the current literature.

Portfolios tilt to more energy-intensive property types

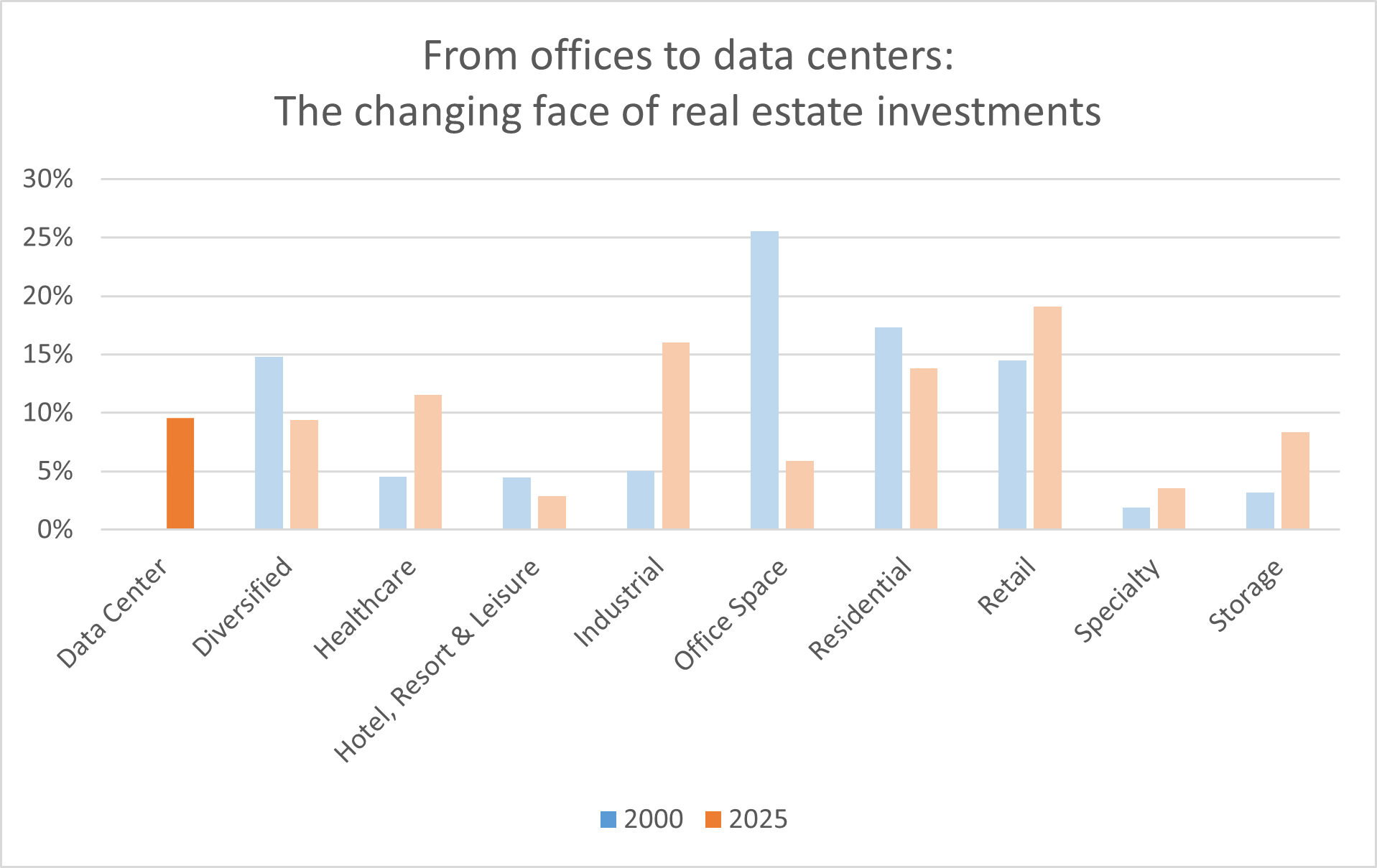

The changing property type preference over time is illustrated in Figure 1, which shows the sector composition of the S&P Global REIT Index[1] in 2000 and 2025.

In 2000, the most dominant property types were offices, residential properties, and retail, making up 25.5%, 17.3%, and 14.5% of the index, respectively. By 2025, office allocations fell to 6%, while sectors such as data centers and storage grew in prominence. Data centers are now classified as a separate category, whereas they were previously combined with other sectors. Data centers comprise 10% of the S&P Global REIT index, with a market value of approximately £147 billion. The private markets have also seen substantial growth. For example, a McKinsey report revealed 209 data center transactions in 2021, with a combined value exceeding $48 billion—an increase of roughly 40% compared to the $34 billion recorded in 2020. Blackstone has a $100 billion data center acquisition pipeline over the next five years, signalling continued market growth for the foreseeable future.

These changes highlight a broader trend of institutional portfolios shifting away from conventional real estate towards alternative assets that respond to modern economic demands, such as digitalisation and the expansion of artificial intelligence, often accompanied by increased energy consumption. Understanding their energy impact will be vital for reconciling sustainability goals with investment strategies as the transition to alternative property types accelerates.

Figure 1

The new asset classes are energy-intensive

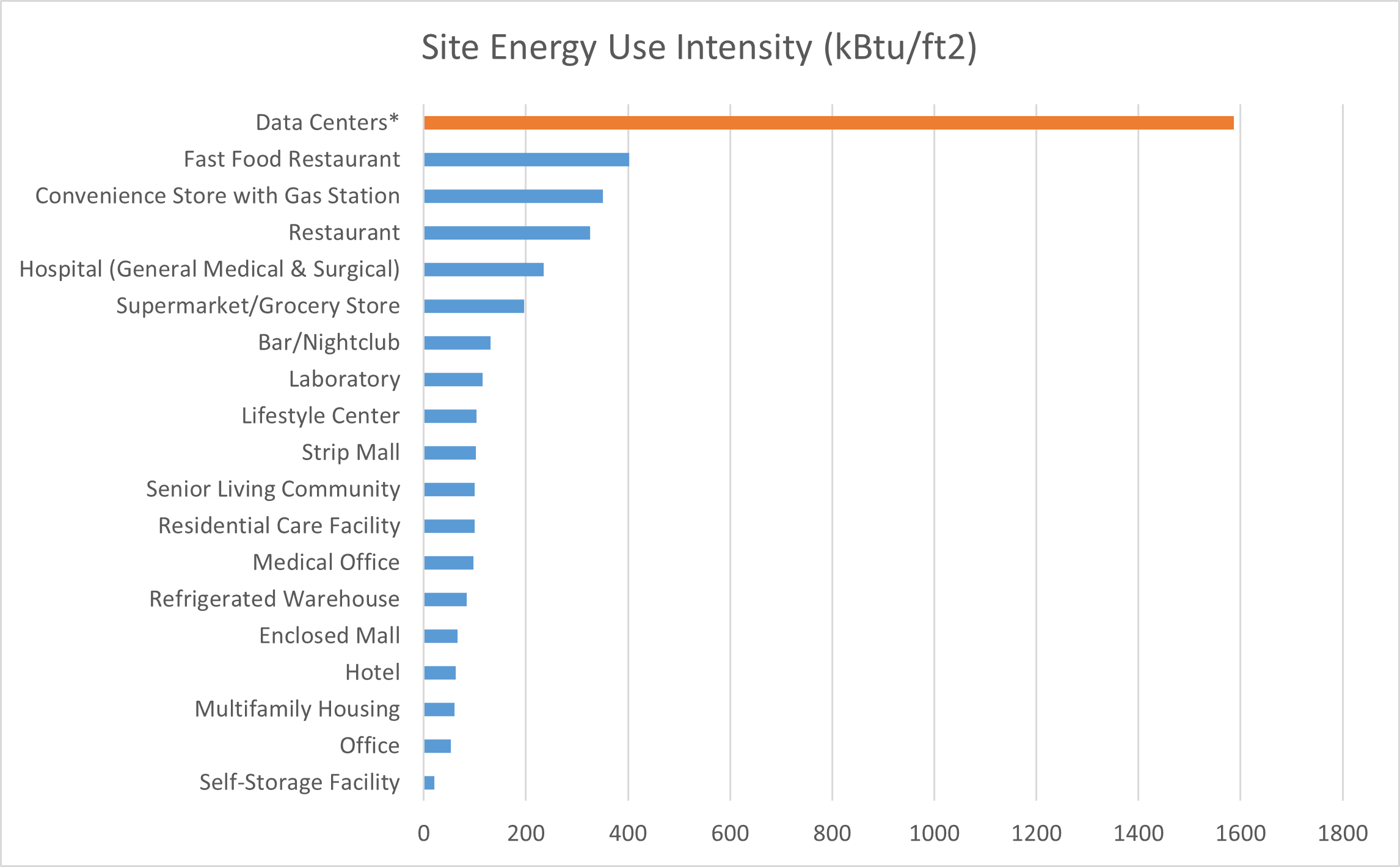

Energy Star provides a framework to help investors and portfolio managers benchmark energy use intensity by property type. Importantly, they stress the need to consider the property type and its usage. Figure 2 illustrates the energy use intensity of various properties according to this framework. The figure reveals that some emerging property types, such as storage, which became significant during the COVID period, consume relatively little energy. Data centers are not included in this framework. However, according to the US Government Department of Energy, data centers consume 10 to 50 times more energy per unit of floor space than a typical commercial office space.

Figure 2. Source: Portfolio manager framework by Energy Star.

Note: ENERGY STAR’s framework does not include data centers as a category. To account for data centers, we rely on assumptions from the U.S. Department of Energy, which estimates that data centers consume 10 to 50 times the energy per square foot compared to typical commercial office space. For this analysis, we use the average of that range, applying a multiplier of 30 to the energy use intensity (EUI) of office spaces.

Data centers are hungry…and thirsty!

The growing prominence of AI technologies like ChatGPT has also increased attention to their energy demands. However, this is less concerning if the energy used is electricity generated from renewable sources. In the race toward sustainability, some of the world’s largest tech companies are setting the standard by committing to 100% renewable energy. Industry giants like Amazon, Apple, Google, Meta, and Microsoft—along with major data center operators such as Iron Mountain and Digital Realty Trust—are making significant strides in reducing their carbon footprint. A prime example is Microsoft’s Cheyenne data center in Wyoming, which runs entirely on renewable energy. However, there is limited data on the extent to which data centers have already transitioned to fully renewable energy sources.

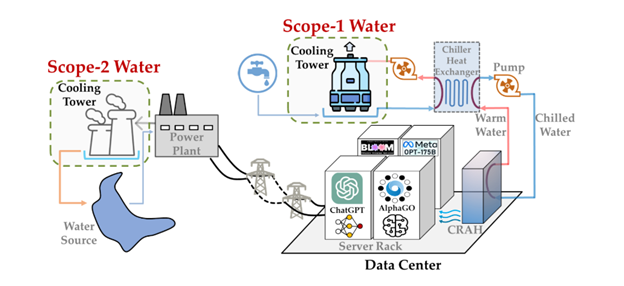

Figure 3: Source

In contrast, the story differs when considering water usage (see Figure 3). The substantial energy consumption of AI servers produces significant heat. Data centers often depend on cooling towers or outside air to dissipate this heat and prevent server overheating. Both methods demand large quantities of clean, fresh water. Consequently, water usage may fall within scope 1 and scope 2 emissions. High water extraction rates typically involve energy-intensive processes such as pumping, treatment, and transportation, which increase CO2 emissions. Furthermore, excessive water extraction can diminish the availability of clean water for surrounding communities, thereby hindering progress towards Sustainable Development Goal (SDG) 6: ensuring the availability and sustainable management of freshwater resources. According to the OECD, by 2027, global water withdrawals related to AI are expected to reach between 4.2 and 6.6 billion cubic metres—equivalent to four to six times Denmark’s annual water withdrawals. For investors with net-zero commitments, this presents a challenge.

Implications for institutional investors

Institutional investors are increasing their allocations to property types such as data centers in response to the digitalisation of the global economy. So, how can the impact on energy usage be balanced? The first step in addressing any issue is acknowledging it and then measuring it. It is essential to enhance the availability and quality of data. Data availability should encompass energy usage, emissions (including Scope 1 and Scope 2), the sources of water extraction, and any potential externality costs imposed on others. That entails reporting the emissions of emerging asset classes like data centers. While this is no small task—given the current limitations in data quality and availability—it is essential for investors to engage effectively and strive to reduce the energy usage of these facilities. Alongside investor efforts to fully comprehend the emissions from the growing presence of data centers in their portfolios, technological advancements will undoubtedly render data centers more energy-efficient and less reliant on fresh water, providing a pathway towards more sustainable solutions.

Disclaimer

The views presented in this article reflect the views of the GREEN Secretariat but do not necessarily represent those of the individual GREEN members.

[1] The S&P Global BMI Indices were introduced to provide a comprehensive benchmarking system for global equity investors. The S&P Global BMI is comprised of the S&P Emerging BMI and the S&P Developed BMI. It covers approximately 10,000 companies in 46 countries. To be considered for inclusion in the index, all listed stocks within the constituent country must have a float market capitalization of at least $100 million. For a country to be admitted, it must be politically stable and have legal property rights and procedures, among other criteria.